Keyword: 相関行列, ロバスト推定

概要

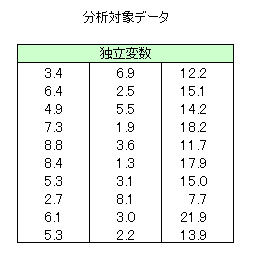

本サンプルは相関行列のロバスト推定値の計算を行うFortranによるサンプルプログラムです。 本サンプルは以下に示されるデータについてロバスト推定値の計算を行います。

※本サンプルはnAG Fortranライブラリに含まれるルーチン g02hmf() のExampleコードです。本サンプル及びルーチンの詳細情報は g02hmf のマニュアルページをご参照ください。

ご相談やお問い合わせはこちらまで

入力データ

(本ルーチンの詳細はg02hmf のマニュアルページを参照)| このデータをダウンロード |

G02HMF Example Program Data

10 3 : N,M

3.4 6.9 12.2

6.4 2.5 15.1

4.9 5.5 14.2

7.3 1.9 18.2

8.8 3.6 11.7

8.4 1.3 17.9

5.3 3.1 15.0

2.7 8.1 7.7

6.1 3.0 21.9

5.3 2.2 13.9 : End of X

1.0 0.0 1.0 0.0 0.0 1.0 : A

0.0 0.0 0.0 : THETA

4.0 2.0 : RUSER

1 0 0.9 0.9 50 5.0E-5 : INDM,NITMON,BL,BD,MAXIT,TOL

- 1行目はタイトル行で読み飛ばされます。

- 2行目は観測値の数(n=10)と独立変数の数(m=3)を指定しています。

- 3〜12行目に独立変数の観測値(x)を指定しています。

- 13行目は下三角行列Aの初期推定値を指定しています。

- 14行目は位置パラメータθの初期推定値を指定しています。

- 15行目はサブルーチンUCVのパラメータ(ruser)を指定しています。

- 16行目は使用される関数vの形式(indm=1:v=1)、出力される反復の情報量(nitmon=0:出力なし)、非対角要素の境界の大きさ(bl=0.9)、対角要素の境界の大きさ(bd=0.9)、最大反復数(maxit=50)、共分散行列の最終推定値の相対精度(tol=5.0E-5)を指定しています。

出力結果

(本ルーチンの詳細はg02hmf のマニュアルページを参照)| この出力例をダウンロード |

G02HMF Example Program Results

G02HMF required 34 iterations to converge

Robust covariance matrix

1 2 3

1 3.2779 -3.6918 4.7391

2 5.2841 -6.4087

3 11.8373

Robust estimates of THETA

5.700

3.864

14.704

- 3行目には収束するのに34回の反復が必要だったことが示されています。

- 5〜9行目にロバスト共分散行列が出力されています。

- 11〜14行目に位置パラメータθのロバスト推定値が出力されています。

ソースコード

(本ルーチンの詳細はg02hmf のマニュアルページを参照)

※本サンプルソースコードは科学技術・統計計算ライブラリである「nAG Fortranライブラリ」のルーチンを呼び出します。

サンプルのコンパイル及び実行方法

| このソースコードをダウンロード |

! G02HMF Example Program Text

! Mark 23 Release. nAG Copyright 2011.

MODULE g02hmfe_mod

! G02HMF Example Program Module:

! Parameters and User-defined Routines

! .. Use Statements ..

USE nag_library, ONLY : nag_wp

! .. Implicit None Statement ..

IMPLICIT NONE

! .. Parameters ..

INTEGER, PARAMETER :: iset = 1, nin = 5, nout = 6

CONTAINS

SUBROUTINE ucv(t,ruser,u,w)

! u function

! .. Implicit None Statement ..

IMPLICIT NONE

! .. Scalar Arguments ..

REAL (KIND=nag_wp), INTENT (IN) :: t

REAL (KIND=nag_wp), INTENT (OUT) :: u, w

! .. Array Arguments ..

REAL (KIND=nag_wp), INTENT (INOUT) :: ruser(*)

! .. Local Scalars ..

REAL (KIND=nag_wp) :: cu, cw, t2

! .. Executable Statements ..

cu = ruser(1)

u = 1.0_nag_wp

IF (t/=0.0_nag_wp) THEN

t2 = t*t

IF (t2>cu) THEN

u = cu/t2

END IF

END IF

! w function

cw = ruser(2)

IF (t>cw) THEN

w = cw/t

ELSE

w = 1.0_nag_wp

END IF

END SUBROUTINE ucv

END MODULE g02hmfe_mod

PROGRAM g02hmfe

! G02HMF Example Main Program

! .. Use Statements ..

USE nag_library, ONLY : g02hmf, nag_wp, x04abf, x04ccf

USE g02hmfe_mod, ONLY : iset, nin, nout, ucv

! .. Implicit None Statement ..

IMPLICIT NONE

! .. Local Scalars ..

REAL (KIND=nag_wp) :: bd, bl, tol

INTEGER :: i, ifail, indm, la, lcov, ldx, &

lruser, m, maxit, n, nadv, nit, &

nitmon

! .. Local Arrays ..

REAL (KIND=nag_wp), ALLOCATABLE :: a(:), cov(:), ruser(:), &

theta(:), wk(:), wt(:), x(:,:)

! .. Executable Statements ..

WRITE (nout,*) 'G02HMF Example Program Results'

WRITE (nout,*)

! Skip heading in data file

READ (nin,*)

! Read in the problem size

READ (nin,*) n, m

ldx = n

lruser = 2

la = ((m+1)*m)/2

lcov = la

ALLOCATE (x(ldx,m),ruser(lruser),cov(lcov),a(la),wt(n),theta(m), &

wk(2*m))

! Read in data

READ (nin,*) (x(i,1:m),i=1,n)

! Read in the initial value of A

READ (nin,*) a(1:la)

! Read in the initial value of THETA

READ (nin,*) theta(1:m)

! Read in the values of the parameters of the ucv functions

READ (nin,*) ruser(1:lruser)

! Read in the control parameters

READ (nin,*) indm, nitmon, bl, bd, maxit, tol

! Set the advisory channel to NOUT for monitoring information

IF (nitmon/=0) THEN

nadv = nout

CALL x04abf(iset,nadv)

END IF

! Compute robust estimate of variance / covariance matrix

ifail = 0

CALL g02hmf(ucv,ruser,indm,n,m,x,ldx,cov,a,wt,theta,bl,bd,maxit,nitmon, &

tol,nit,wk,ifail)

! Display results

WRITE (nout,99999) 'G02HMF required ', nit, ' iterations to converge'

WRITE (nout,*)

FLUSH (nout)

ifail = 0

CALL x04ccf('Upper','Non-Unit',m,cov,'Robust covariance matrix',ifail)

WRITE (nout,*)

WRITE (nout,*) 'Robust estimates of THETA'

WRITE (nout,99998) theta(1:m)

99999 FORMAT (1X,A,I0,A)

99998 FORMAT (1X,F10.3)

END PROGRAM g02hmfe