Keyword: 一変量時系列, GARCH, 非対称, パラメータ推定

概要

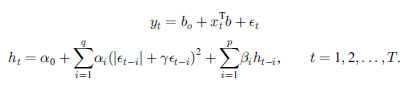

本サンプルは一変量のAGARCH type2プロセスのパラメータ推定を行うFortranによるサンプルプログラムです。 本サンプルでは以下に示される時系列を分析対象とし下記の式で表されるAGARCH type2プロセスのパラメータ推定を行います。

※本サンプルはnAG Fortranライブラリに含まれるルーチン g13fcf() のExampleコードです。本サンプル及びルーチンの詳細情報は g13fcf のマニュアルページをご参照ください。

ご相談やお問い合わせはこちらまで

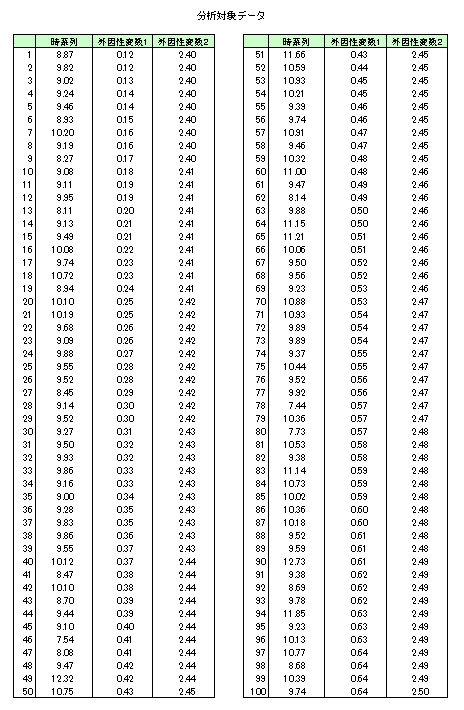

入力データ

(本ルーチンの詳細はg13fcf のマニュアルページを参照)| このデータをダウンロード |

G13FCF Example Program Data 100 1 2 :: NUM,MN,NREG 8.87 9.82 9.02 9.24 9.46 8.93 10.20 9.19 8.27 9.08 9.11 9.95 8.11 9.13 9.49 10.08 9.74 10.72 8.94 10.10 10.19 9.68 9.09 9.88 9.55 9.52 8.45 9.14 9.52 9.27 9.50 9.93 9.86 9.16 9.00 9.28 9.83 9.86 9.55 10.12 8.47 10.10 8.70 9.44 9.10 7.54 8.08 9.47 12.32 10.75 11.66 10.59 10.93 10.21 9.39 9.74 10.91 9.46 10.32 11.00 9.47 8.14 9.88 11.15 11.21 10.06 9.50 9.56 9.23 10.88 10.93 9.89 9.89 9.37 10.44 9.52 9.92 7.44 10.36 7.73 10.53 9.38 11.14 10.73 10.02 10.36 10.18 9.52 9.59 12.73 9.38 8.69 9.78 11.85 9.23 10.13 10.77 8.68 10.39 9.74 :: End of Y 0.12 2.40 0.12 2.40 0.13 2.40 0.14 2.40 0.14 2.40 0.15 2.40 0.16 2.40 0.16 2.40 0.17 2.40 0.18 2.41 0.19 2.41 0.19 2.41 0.20 2.41 0.21 2.41 0.21 2.41 0.22 2.41 0.23 2.41 0.23 2.41 0.24 2.41 0.25 2.42 0.25 2.42 0.26 2.42 0.26 2.42 0.27 2.42 0.28 2.42 0.28 2.42 0.29 2.42 0.30 2.42 0.30 2.42 0.31 2.43 0.32 2.43 0.32 2.43 0.33 2.43 0.33 2.43 0.34 2.43 0.35 2.43 0.35 2.43 0.36 2.43 0.37 2.43 0.37 2.44 0.38 2.44 0.38 2.44 0.39 2.44 0.39 2.44 0.40 2.44 0.41 2.44 0.41 2.44 0.42 2.44 0.42 2.44 0.43 2.45 0.43 2.45 0.44 2.45 0.45 2.45 0.45 2.45 0.46 2.45 0.46 2.45 0.47 2.45 0.47 2.45 0.48 2.45 0.48 2.46 0.49 2.46 0.49 2.46 0.50 2.46 0.50 2.46 0.51 2.46 0.51 2.46 0.52 2.46 0.52 2.46 0.53 2.46 0.53 2.47 0.54 2.47 0.54 2.47 0.54 2.47 0.55 2.47 0.55 2.47 0.56 2.47 0.56 2.47 0.57 2.47 0.57 2.47 0.57 2.48 0.58 2.48 0.58 2.48 0.59 2.48 0.59 2.48 0.59 2.48 0.60 2.48 0.60 2.48 0.61 2.48 0.61 2.48 0.61 2.49 0.62 2.49 0.62 2.49 0.62 2.49 0.63 2.49 0.63 2.49 0.63 2.49 0.64 2.49 0.64 2.49 0.64 2.49 0.64 2.50 :: End of X 'T' 1 1 :: DIST,IP,IQ T T 200 0.00001 :: COPTS,MAXIT,TOL 0.05 :: ALPHA_0 0.05 :: ALPHA_I 0.40 :: BETA_I -0.20 :: GAMMA 2.60 :: DF 1.50 :: MEAN 4 :: NT

- 1行目はタイトル行で読み飛ばされます。

- 2行目に時系列のデータの数(num=100)、切片がモデルに含まれかどうか(mn=1:含まれる)、 回帰係数の数(nreg=2)を指定しています。

- 3〜22行目に時系列の観測値(y)を指定しています。

- 23〜72行目に時間依存の外因性変数の要素(x)を指定しています。

- 73行目に分布の種類(dist='T')、係数βの数(ip=1)、係数αの数(iq=1)を指定しています。

- 74行目に定常状態が強制されるかどうか(copts(1)=T:強制される)、ルーチンが初期のパラメータ推定を与えるかどうか(copsts(2)=T:与える)、最大反復数(maxit=200)、最適化ルーチンで使用される許容値(tol=0.00001)を指定しています。

- 75行目に係数α0(alpha_0)を指定しています。

- 76行目に係数α1(alpha_i)を指定しています。

- 77行目に係数β1(beta_i)を指定しています。

- 78行目に非対称パラメータγ(gamma)を指定しています。

- 79行目に自由度(df)を指定しています。

- 80行目に切片(mean)を指定しています。

- 81行目に予測期間(nt)を指定しています。

出力結果

(本ルーチンの詳細はg13fcf のマニュアルページを参照)| この出力例をダウンロード |

G13FCF Example Program Results

Parameter Standard

estimates errors

Alpha0 6.82 1.68

Alpha1 0.00 1.00

Beta1 0.00 3.17

Gamma -0.36 1.01

DF 2.10 0.33

B0 -25.14 4.80

B1 -0.95 0.90

B2 14.41 2.08

Volatility forecast = 6.82

- 5行目に係数α0のパラメータ推定値、標準誤差が出力されています。

- 6行目に係数α1のパラメータ推定値、標準誤差が出力されています。

- 8行目に係数β1のパラメータ推定値、標準誤差が出力されています。

- 10行目に非対称パラメータγのパラメータ推定値、標準誤差が出力されています。

- 12行目に自由度のパラメータ推定値、標準誤差が出力されています。

- 14行目に切片のパラメータ推定値、標準誤差が出力されています。

- 15〜16行目に線形回帰係数のパラメータ推定値、標準誤差が出力されています。

- 19行目には4step先のボラティリティ予測値が出力されています。

ソースコード

(本ルーチンの詳細はg13fcf のマニュアルページを参照)

※本サンプルソースコードは科学技術・統計計算ライブラリである「nAG Fortranライブラリ」のルーチンを呼び出します。

サンプルのコンパイル及び実行方法

| このソースコードをダウンロード |

PROGRAM g13fcfe

! G13FCF Example Program Text

! Mark 23 Release. nAG Copyright 2011.

! .. Use Statements ..

USE nag_library, ONLY : g13fcf, g13fdf, nag_wp

! .. Implicit None Statement ..

IMPLICIT NONE

! .. Parameters ..

INTEGER, PARAMETER :: nin = 5, nout = 6

! .. Local Scalars ..

REAL (KIND=nag_wp) :: gamma, hp, lgf, tol

INTEGER :: i, ifail, ip, iq, l, ldcovr, ldx, &

lwork, maxit, mn, npar, nreg, nt, &

num, pgamma, tdx

LOGICAL :: tdist

CHARACTER (1) :: dist

! .. Local Arrays ..

REAL (KIND=nag_wp), ALLOCATABLE :: covr(:,:), et(:), fht(:), ht(:), &

sc(:), se(:), theta(:), work(:), &

x(:,:), yt(:)

LOGICAL :: copts(2)

! .. Intrinsic Functions ..

INTRINSIC max

! .. Executable Statements ..

WRITE (nout,*) 'G13FCF Example Program Results'

WRITE (nout,*)

! Skip heading in data file

READ (nin,*)

! Read in the problem size

READ (nin,*) num, mn, nreg

ldx = num

tdx = max(nreg+mn,1)

ALLOCATE (yt(num),x(ldx,tdx))

! Read in the series

READ (nin,*) yt(1:num)

! Read in the exogenous variables

IF (nreg>0) THEN

READ (nin,*) (x(i,1:nreg),i=1,num)

END IF

! Read in details of the model to fit

READ (nin,*) dist, ip, iq

! Read in control parameters

READ (nin,*) copts(1:2), maxit, tol

! Calculate NPAR

npar = 2 + iq + ip + mn + nreg

IF (dist=='T' .OR. dist=='t') THEN

npar = npar + 1

tdist = .TRUE.

ELSE

tdist = .FALSE.

END IF

ldcovr = npar

lwork = (nreg+3)*num + npar + 403

ALLOCATE (theta(npar),se(npar),sc(npar),covr(ldcovr,npar),et(num), &

ht(num),work(lwork))

! Read in initial values

! alpha_0

READ (nin,*) theta(1)

l = 2

! alpha_i

IF (iq>0) THEN

READ (nin,*) theta(l:(l+iq-1))

l = l + iq

END IF

! beta_i

IF (ip>0) THEN

READ (nin,*) theta(l:(l+ip-1))

l = l + ip

END IF

! gamma

READ (nin,*) theta(l)

pgamma = l

l = l + 1

! degrees of freedom

IF (tdist) THEN

READ (nin,*) theta(l)

l = l + 1

END IF

! mean

IF (mn==1) THEN

READ (nin,*) theta(l)

l = l + 1

END IF

! Regression parameters and pre-observed conditional variance

IF ( .NOT. copts(2)) THEN

READ (nin,*) theta(l:(l+nreg-1))

READ (nin,*) hp

END IF

! Fit the GARCH model

ifail = 0

CALL g13fcf(dist,yt,x,ldx,num,ip,iq,nreg,mn,npar,theta,se,sc,covr, &

ldcovr,hp,et,ht,lgf,copts,maxit,tol,work,lwork,ifail)

! Read in forecast horizon

READ (nin,*) nt

ALLOCATE (fht(nt))

! Extract the estimate of the asymmetry parameter from theta

gamma = theta(pgamma)

! Calculate the volatility forecast

ifail = 0

CALL g13fdf(num,nt,ip,iq,theta,gamma,fht,ht,et,ifail)

! Output the results

WRITE (nout,*) ' Parameter Standard'

WRITE (nout,*) ' estimates errors'

! Output the coefficient alpha_0

WRITE (nout,99999) 'Alpha', 0, theta(1), se(1)

l = 2

! Output the coefficients alpha_i

IF (iq>0) THEN

WRITE (nout,99999) ('Alpha',i-1,theta(i),se(i),i=l,l+iq-1)

l = l + iq

END IF

WRITE (nout,*)

! Output the coefficients beta_j

IF (ip>0) THEN

WRITE (nout,99999) (' Beta',i-l+1,theta(i),se(i),i=l,l+ip-1)

l = l + ip

WRITE (nout,*)

END IF

! Output the estimated asymmetry parameter, gamma

WRITE (nout,99998) ' Gamma', theta(l), se(l)

WRITE (nout,*)

l = l + 1

! Output the estimated degrees of freedom, df

IF (dist=='T') THEN

WRITE (nout,99998) ' DF', theta(l), se(l)

WRITE (nout,*)

l = l + 1

END IF

! Output the estimated mean term, b_0

IF (mn==1) THEN

WRITE (nout,99999) ' B', 0, theta(l), se(l)

l = l + 1

END IF

! Output the estimated linear regression coefficients, b_i

IF (nreg>0) THEN

WRITE (nout,99999) (' B',i-l+1,theta(i),se(i),i=l,l+nreg-1)

END IF

WRITE (nout,*)

! Display the volatility forecast

WRITE (nout,*)

WRITE (nout,99997) 'Volatility forecast = ', fht(nt)

WRITE (nout,*)

99999 FORMAT (1X,A,I0,1X,2F16.2)

99998 FORMAT (1X,A,1X,2F16.2)

99997 FORMAT (1X,A,F12.2)

END PROGRAM g13fcfe